Imagine paying $1500/month for rent in 2021 and getting a renewal letter for $2079. We hope you enjoyed last week’s edition where we talked about What Opportunities Do Lenders Miss Out On By Not Focusing On Credit? This week we’re bringing you:

eClosing, AI, Portfolio, and Non-QM Products; Conforming Updates

At the Ides of March, inflation is pervasive. Today rumors are swirling that Tom Brady ended his retirement because of not being able to afford to retire given the price of gasoline (more in Capital Markets section below), and I head to the home of Holiday Inn: Memphis, Tennessee. (Yes, the title of the song is a little misleading; it spot-on focuses on Tennessee.)

Millions in China have re-entered COVID lockdown, once again impacting the supply chain. Russia continues to batter Ukraine, with its terrible loss of human life, impacting the worldwide price of oil and other commodities. We’re watching it all happen in real time, through the use of technology.

In this country, Census Bureau construction surveys (brought to you since 1959) are being upgraded with satellite images to provide instant updates on projects at every stage of construction from start to finish down to the county and metro level for the first time. The changes will modernize nearly every aspect of the construction data the Census Bureau releases, including New Residential Construction, one of the most timely and leading official measures of the current condition of the U.S. economy. The first estimates from a new sample design were published February 17, and the local and county level estimates from the redesigned Monthly Building Permit Survey were published for the first time February 24.

Lender and broker products & services

Last month, Freddie Mac announced the launch of its Loan Product Advisor® (LPASM) verification of income (VOI) solution, which allows the 93% of Americans paid via direct deposit to authorize lender assessment of income using direct-source bank data. The culmination of years of lender-informed development, high adoption of Freddie Mac’s technology tools has been proven to deliver substantial cost savings for lenders to the tune of $2,200 per loan. FormFree is proud to be one of the first authorized report providers for this revolutionary solution, and sees this advancement as an opportunity to make the income verification process easier, safer, and more inclusive for everyone. Drop by booth #326 at ICE Experience to learn more about how FormFree’s support of Freddie Mac’s VOI initiative can help streamline the underwriting process and expand access to sustainable homeownership.

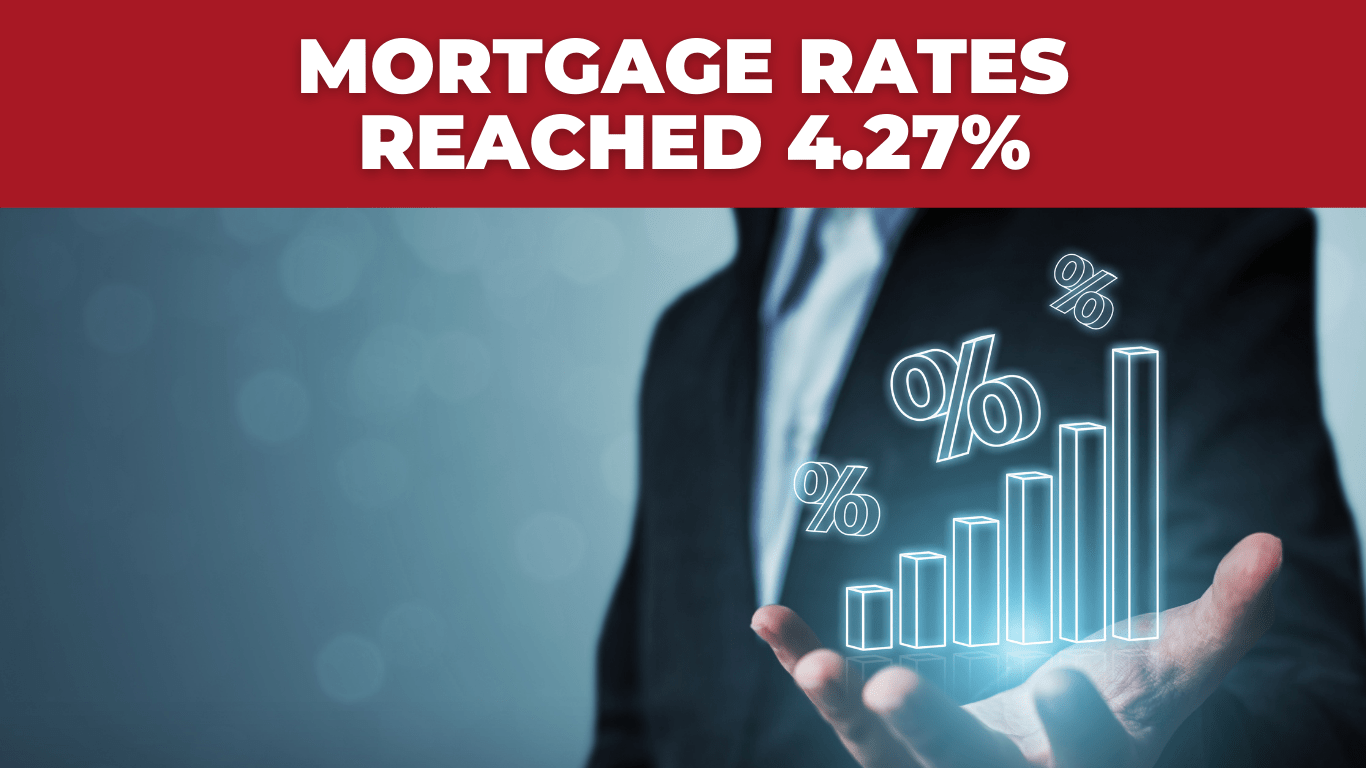

Mortgage applications drop as rates spike

Mortgage rates reached 4.27%, the highest level since May 2019

Interest in residential mortgages fell 1.2% for the week ending March 11 as mortgage rates rose to their highest levels since May 2019, according to the Mortgage Bankers Association‘s latest survey.

“Mortgage rates continue to be volatile due to the significant uncertainty regarding Federal Reserve policy and the situation in Ukraine,” said Joel Kan, associate vice president of economic and industry forecasting for the MBA. “Investors are weighing the impacts of rapidly increasing inflation in the U.S. and many other parts of the world against the potential for a slowdown in economic growth due to a renewed bout of supply-chain constraints.”

Mortgage rates, which recently hit 4.27% for 30-year-fixed rate mortgages, are now a full percentage point higher than a year ago. That’s led to a significant decline in refinance activity, both for conventional and government loans.

According to the MBA, refi applications fell 3% from the prior week and were down 49% from a year ago. The seasonally adjusted purchase index increased 1% from one week earlier; the unadjusted purchase index increased 2% from the prior week but was 8% lower than the same week a year ago, largely due to a decline in inventory.

“Purchase applications slightly increased, with both conventional and VA loan applications seeing gains,” said Kan. “The average purchase application loan size remained elevated at $453,200 – the second- highest amount in MBA’s survey.”

The MBA found that the adjustable-rate mortgage share of the activity increased to 5.6% of total applications.

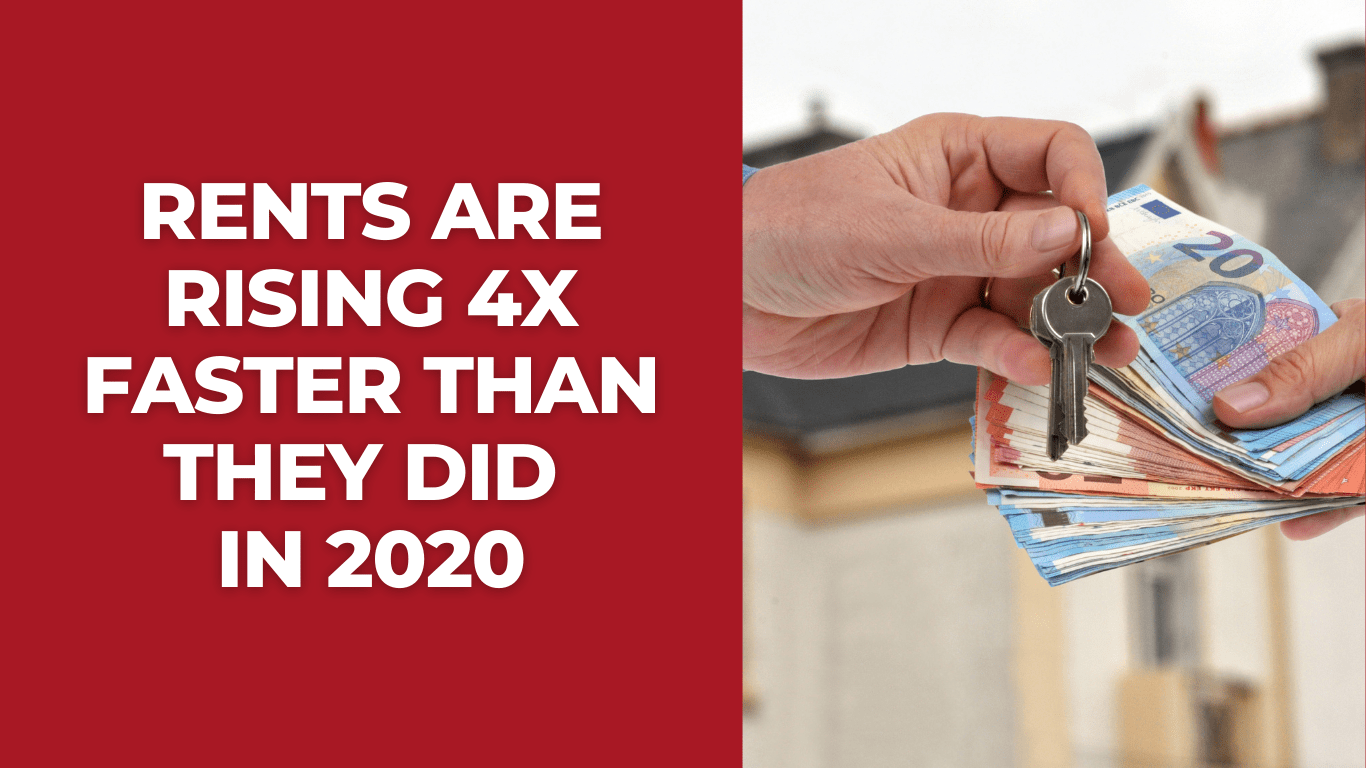

Rents Are Rising 4 Times Faster Than They Did in 2020

Imagine paying $1500/month for rent in 2021 and getting a renewal letter for $2079. That’s the reality for those living in the metropolitan area where rental prices are accelerating the fastest according to the Single-Family Rent Index (SFRI) released today month by CoreLogic.

While the 38.6% seen in Miami was by far the highest annual change, other metros were nonetheless well above 2020’s levels. In fact, rental prices are now appreciating more than 4 times faster compared to 2020’s average (12.6% vs 2.6% in 2020).

Keep in mind that the “4 times faster” comparison is a bit misleading because we’re taking the very hottest month and comparing it to an average of 12 months. If we instead simply use the latest month of 2020 as a baseline, the thesis becomes something more like “rental price appreciation remains in double digit territory.” Specifically, December’s year-over-year change was 12.0% compared to January’s 12.6%.

One notable shift over the past several months has been the ability of the “attached” home sector (condos/townhomes) to match the pace of the detached single family residence.

Rent price appreciation has been broad-based as well, with both low and mid tier homes at 12% and 12.2% respectively. Not pictured in the chart above, middle-priced tiers led the charge with both “lower-middle” (75%-100% of regional median) and “higher-middle” (100%-125% of regional median) coming in at 13.3% and 13.4% respectively.

Finding highly affordable leads to keep sales coming in

At iLeads, we have many great solutions for mortgage LO’s at a low cost. If you’d like to see how we can help you bring in consistent sales for a great price, give us a call at (877) 245-3237!

We’re free and are taking phone-calls from 7AM to 5PM PST, Monday through Friday.

You can also schedule a call here.