Press Releases

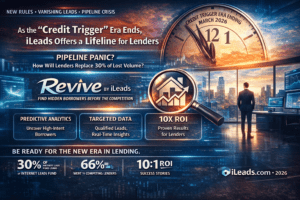

As the “Credit Trigger” Era Ends This March, iLeads Offers a Proven Lifeline for Lenders

With regulatory changes poised to wipe out pipeline volume, the “Revive” platform uses predictive analytics to uncover high-intent borrowers before the competition calls. Newport Beach,