Welcome back to iLeads Mortgage Market Minute, where we bring you the latest, most relevant news regarding the mortgage market. We hope you enjoyed last week’s edition where we talked about MBA Predicts Record Purchase Mortgage Volume In 2021. This week we’re bringing you The Housing Market:

September Home Price Gains Blow Away Forecasts*

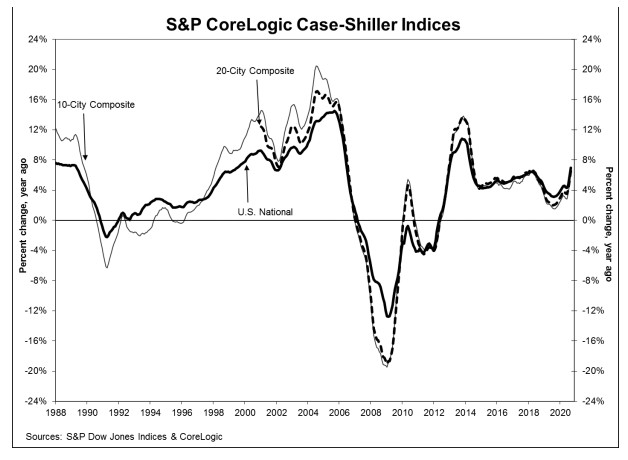

Annual price increases in September were quite literally off the charts. Both the S&P CoreLogic Case-Shiller National Index and the Housing Market Index from the Federal Housing Finance Agency (FHFA) recorded an annual appreciation of at least 7 percent.

The Case-Shiller National Index, which covers all nine U.S. census divisions, reported a 7.0 percent annual gain in September, up from the August increase of 5.8 percent. The National Index posted 1.2 percent month-over-month growth before seasonal adjustment and 1.4 percent afterward.

As has been the case since the beginning of the pandemic, housing data from Wayne County, Michigan where Detroit is located has been insufficient to include the city in the indices. The 10-City Composite annual increase came in at 6.2 percent and the 20 City at 6.6 percent. The two composites had appreciated in August by 4.9 percent and 5.3 percent, respectively. On a monthly basis, the 10-City increased 1.3 percent before the adjustment and 1.2 percent afterward, while the 20 City’s gains were the reverse, rising 1.2 percent before the adjustment and 1.3 percent afterward. In September, all 19 cities (excluding Detroit) reported increases before and after seasonal adjustment.

The 20-City Composite is the Case-Shiller Component about which analysts usually offer a forecast. They badly undershot the mark for September. Analysts polled by Econoday were expecting an annual increase of 5.4 percent, Trading Economics predicted a 5.1 percent gain.

Low, low mortgage rates make 19.4 million eligible for refi*

Homeowners could save an aggregate of $5.98 billion per month

As mortgage rates stay below 3% for the 17th consecutive week, a Black Knight report released Friday found that the number of “high quality” refinance candidates continues to climb. According to the report, a whopping 19.4 million homeowners are now in a position to save through refis – the most in history.

Black Knight’s report views prime candidates as 30-year mortgage-holders who have at least 20% equity in their homes, credit scores of 720 or higher, are current on their payments, and who stand to cut their first lien rates at least 0.75% by refinancing.

Looking at current mortgage rates, Black Knight estimates those 19.4 million candidates can save an average of $309 per month by refinancing. If every qualified borrower did so, the aggregate potential savings would be the most ever recorded – a massive $5.98 billion.

Some borrowers could save even more. With today’s rates, the report found 4.5 million could save at least $400 a month, while 2.7 million could save an average of $500 or more.

Regionally, California led the nation in the number of refi candidates – a total of 3 million could potentially save on average $420 a month. Florida recorded 1.4 million borrowers who could do the same, followed by 1.3 million in Texas and 1.1 million in New York.

Pandemic Causing Almost Half of Americans to Consider a Move*

A recent survey by Lending Tree found that nearly half of Americans are thinking about moving in the not-to-distant future and it appears that the COVID-19 pandemic may be at least part of their motivation. Crissinda Ponder writes that the health crisis has affected nearly every aspect of daily life, and with 11 million Americans unemployed, residents make an exodus from major cities, a desire for more living space. There is no reason to think that housing choices would be any less affected.

The Lending Tree survey covered 2,000 consumers and 46 percent said they were thinking about relocating within the next year. Twenty-seven percent are considering a new home in their current area, with a primary motivation of reducing their living expenses. Another 12 percent would consider a nearby city, while 8 percent would like to move to a new state.

Reducing living expenses was cited by 44 percent of all respondents. Other reasons frequently given were:

- “My current home is too small” (27 percent)

- “I’m looking for different features” (27 percent)

- “I’d rather live in a different part of town” (12 percent)

Renters also frequently said they didn’t like the way their property was being managed.

How The New Loan Limits Affect Mortgage Rates*

If you follow the MBS Commentary channel on this site, you will have already seen most of the following, but it’s relevant for consumers as well. As far as mortgage rates are concerned, the increase in conforming loan limits doesn’t have a direct impact, but it does change rate availability for those seeking certain loan amounts. There’s a link below where you can see exactly what the new loan limit is for any given county.

If you’d like to read the official FHFA press release, here you go, but here’s the skinny on the new conforming loan limit of $548,250 for 2021, up from $510,400 in 2020.

Which loans does this apply to?

Conventional, conforming loans (those sold to or securitized by Fannie Mae and Freddie Mac, which is a vast majority of the market), both refinances and purchases

Does this apply to FHA/VA/USDA loans?

Not immediately, and not equally. FHA will use the new number to announce its own loan limit increases in a week or two. When that happens, you can always use this page to determine your county’s limit. VA is a bit different depending on how much entitlement you have (read more on the VA site).

What’s the benefit of having a conforming loan amount?

Conforming loans have the lowest effective rates (FHA rates may be lower, but they carry mortgage insurance). They also have different qualification standards (typically “easier”) than loans for higher amounts, but this can depend on the lender and your scenario.

Here’s what to expect from a Biden administration regarding housing*

Likely candidates for key positions, and what regulation focus to expect

We are now under 60 days remaining until we have President Biden and Vice President Harris leading a new administration in D.C. Beyond any political views of the election and the ensuing drama, the industry is asking: What will a Biden regime mean to housing and mortgages? How should we think about regulation, the GSEs, HUD, and more?

Here are a few thoughts to consider as to what the next four years may look like.

In a general sense, Democratic regimes tend to be more bullish for government support to housing, while Republican ones are more bullish for lowering the aggressiveness of regulators and oversight. While not a universal truth, we can all remember the eight years under President Obama and the impact of a new, aggressive, regulator tasked under a congressional legal mandate to implement the required rules set forth in Dodd Frank.

Those were challenging years, and while the implementation was hard and every rule has imperfections, today we are past those statutory obligations as all the rules required are now in place. For that reason, I do not expect the aggressive regulatory posture overseeing mortgage lenders to be like it was under Obama.

So how should we think about a Biden administration? Here are some key elements:

Transition: At this point, the transition team has assigned ‘Agency Review Teams’ to each regulator and, not surprisingly, there are many familiar names on these teams that will affect housing. The HUD team is headed by a former political from the Obama years, Erica Poethig, and the team consists of several others from that administration, as well as names like Julia Gordan, a long-time credible consumer advocate for housing policy in Washington.

Treasury, NEC, CFPB, and more have known similar members. Treasury, for example, has Helen Kanovsky. Kanovsky was the general counsel at HUD during both Secretary Donovan and Castro’s tenure. She then joined the Mortgage Bankers Association as the general counsel there until her recent retirement.

Key Takeaway: There are two. First is the noticeable absence of a transition team for FHFA. Second, there is a deep bench of knowledgeable experts who will help bring experience to the task of filling key positions, evaluating policies made and proposed, and more.

The housing market is hot, but not in a bubble*

But rising home prices are a concern

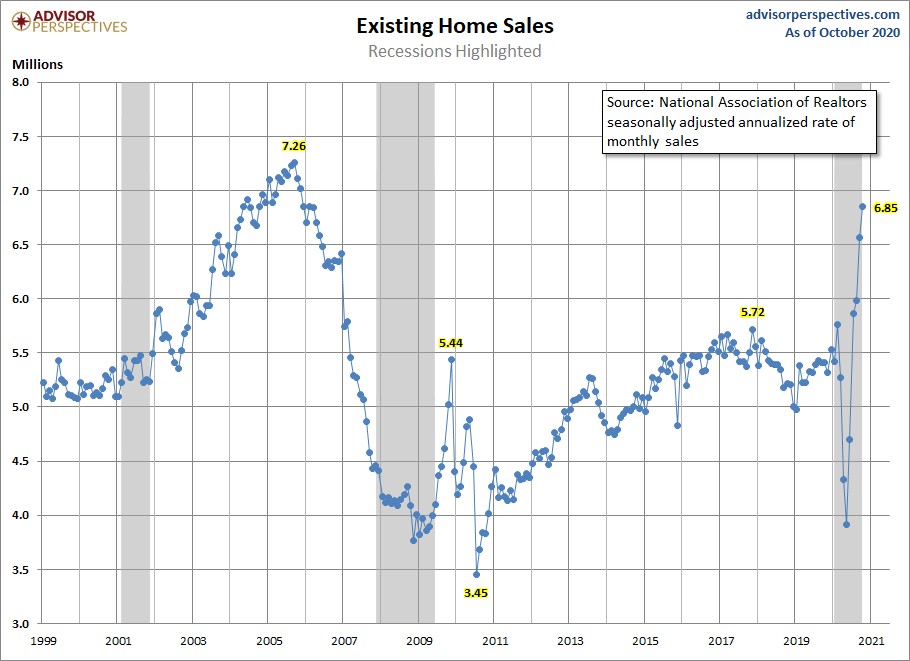

Existing home sales came in at a whopping 6,850,000, beating estimates with the highest print since 2006. Days on market fell from 36 days to 21 days on a year-over-year basis. Cash buyers remain at a historically high level of 19%, the same as last year, while sales grew 26.6% year over year. We have done a lot running around with the existing home sales data to be up just 2.4% year to date.

The housing market is clearly hot.

While we celebrate these strong numbers, keep in mind these three points:

First, expect the data to moderate, so don’t freak out when we see the rate of growth cool down. A normal trend will eventually materialize. You may be told that future moderation indicates “cracks in the housing market, but don’t buy into it. I previously wrote that if we really saw cracks in the housing market, these are a few indicators to track and to beware of doom and gloom housing headlines.

Second, if the next existing home sales report misses expectations, you may be told that this is due to a lack of inventory. Don’t listen. Remember, lower inventory tends to go with higher sales — and higher sales means folks are buying homes…therefore…I know you are following me here… there must be homes to buy.

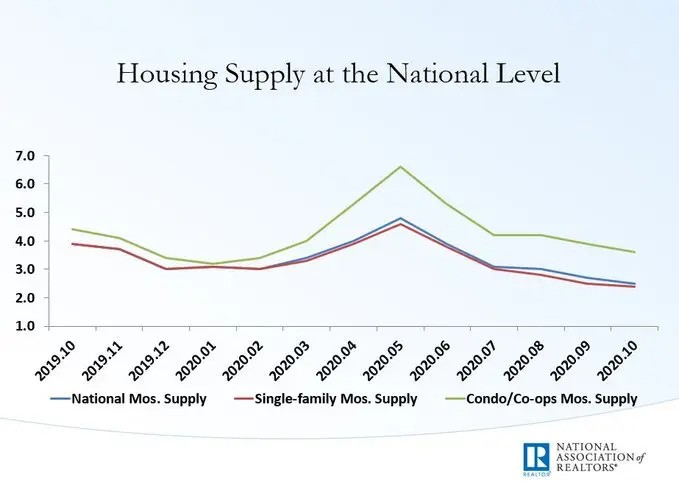

Unsold inventory sits at an all-time low 2.5-month supply at the current sales pace, down from 2.7 months in September and down from the 3.9-month figure recorded in October 2019. Inventory is tight, but it’s not non-existent. Tight inventory also encourages builders to create more inventory.

Finding highly affordable leads to keep sales coming in

At iLeads, we have many great solutions for mortgage LO’s at a low cost. If you’d like to see how we can help you bring in consistent sales for a great price, give us a call at (877) 245-3237!

We’re free and are taking phone-calls from 7AM to 5PM PST, Monday through Friday.

You can also schedule a call here.